Ole_CNX

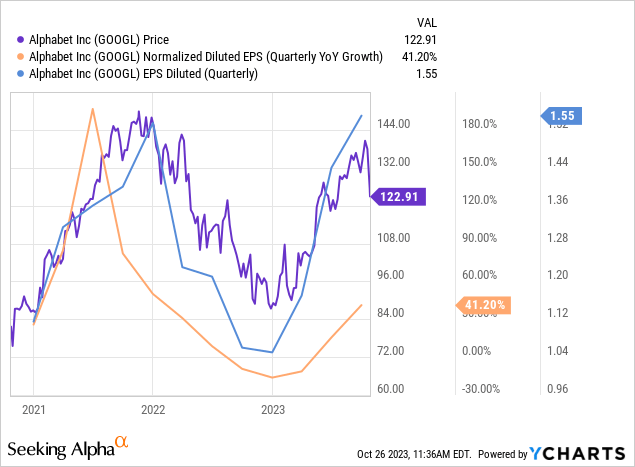

Alphabet (Nasdaq: GOOG) (GOOGLE) reported its Q3 2023 revenue on October 24, 2023, which strongly beat analyst consensus estimates for revenue and revenue driven by strong advertising and YouTube results. However, investors were disappointed with the results of the company’s cloud business. Investors reacted Shares fell nearly 10 percent the next day to close at $126.67.

Any pullback in the share price presents investors with an excellent opportunity to invest in a company that is ideally positioned to become one of the Top Artificial Intelligence (“AI”) Leaders.. Alphabet has a significant advantage in AI and the financial resources to maintain its position as one of the leading innovators in the space. Research and development of artificial intelligence is expensive and requires huge investment. As of the end of September, it had $120 billion in cash and short-term investments against $13.781 billion in long-term debt. Generated approximately $78 billion in free 12 months cash flow, mainly from its profitable search business model. Only a handful of companies worldwide have the financial resources to invest in AI at Alphabet’s pace.

although Microsoft (MSFT) and OpenAI grabbed many of the headlines around generative AI and large-scale language models (LLM), Alphabet has arguably been the most aggressive investor in AI and autonomous technologies over the past decade. Google Alphabet started working Self-driving cars In 2009. The company bought Eight robotics companies Within six months in 2013 and purchase DeepMind in 2014. It was one of the first major tech companies to transform from a mobile-first company to a corporation The first artificial intelligence company, made this announcement in 2016. Transformer invented the leading ChatGPT technology. In 2017. So the narrative that Microsoft is way ahead of Alphabet in AI may be overblown.

If you’re a growth investor looking for one of the best ways to invest in AI over the next decade, now is the time to take a serious look at Alphabet.

The company is injecting artificial intelligence into all its products

Ever since Microsoft and OpenAI woke the AI giant from its slumber with the introduction of ChatGPT in November 2022, Alphabet has been ramping up to add productive AI products to its consumer and enterprise businesses. One of the first places Alphabet applied this new technology was in search. When OpenAI introduced ChatGPT, a former Google employee, Paul Buchheit, the creator of Gmail and Google AdSense, promoted the idea that OpenAI’s new AI technology would be fast. Eliminate Google Search.

Alphabet quickly countered the theory that Microsoft could quickly kill Google Search by adding ChatGPT to Bing. Productive artificial intelligence capabilities To search to create Seeking productive experience (“SGE”). This new product improves Google search and competes with Bing-ChatGPT combination. So far, there’s little evidence that Microsoft is gaining ground in search. said Sundar Pichai, Chief Executive Officer (“CEO”). Alphabet’s third quarter earnings call:

By using generative AI in search, we can meet a wider range of information needs and answer new types of questions, including questions that benefit from multiple perspectives. We’re finding more links to SGE and linking to a wider range of resources on the results page, creating new opportunities for content discovery.

Source: Alphabet text of the third quarter of 2023

The company is also adding Bard to more areas of search. Bard integrates with Workspace, Maps, YouTube, and Google Flights and Hotels. The alphabet is also added Bard to Google Assistantthereby introducing generative AI to Android – an advantage over Microsoft, which lacks a viable mobile platform.

Last but not least, it has positioned itself as a premier AI infrastructure company through its cloud assets. Through Google Cloud Platform (GCP), enterprises, developers, data scientists, and engineers can build, train, test, track, fine-tune, and deploy machine learning and artificial intelligence models. GCP is attractive to early-stage AI companies and large enterprises alike. CEO Pichai said The following during the profit call:

Today, more than 60% of the world’s 1000 largest companies are Google Cloud customers… [And] More than half of all productive AI startups are Google Cloud customers. This includes AI21 Labs, Contextual, Elemental Cognition, Rytr, and more.

Source: Text of Alphabet’s third quarter 2023 earnings call

Alphabet has made a big bet on generative artificial intelligence, which will help Google Cloud make headway Amazon (AMZN) AWS and Microsoft Azure.

However, the cloud business will lay an egg in the third quarter

So far, Alphabet’s big bet on artificial intelligence in the cloud hasn’t paid off. Investors expected a lot from the cloud business in recent quarters, especially after its recent gains. Operating profitability Earlier this year, a masterpiece of some thought It was impossible. However, the cloud grew less than investors expected in the third quarter. Google Cloud revenue rose 22% to $8.41 billion, beating Wall Street It is estimated at 8.64 billion dollars. Microsoft reported earnings on the same day with increased revenues from its Intelligent Cloud and Azure public cloud segments. consensus analyst estimates. KeyBanc Capital Markets Analyst Justin Peterson reported Investor Business Daily It is stated in a report“Google Cloud appears to be ceding market share to Microsoft Azure.”

Alphabet has invested heavily in building artificial intelligence capabilities because it believes the technology can help it differentiate its cloud platform from competitors and attract new customers. Therefore, Google Cloud’s lack of progress in gaining share from Microsoft’s intelligent cloud makes it difficult. “The third quarter year-over-year growth rate reflects the impact of our customer optimization efforts,” Chief Financial Officer (“CFO”) Ruth Porat said on the company’s third quarter earnings call. During 2022, “customer optimization efforts” often meant companies were looking for ways to reduce their cloud costs — a poor scenario for growing Google Cloud sales.

Some additional risks

The most important risk investors should be aware of is that Alphabet is facing two antitrust lawsuits by the US Department of Justice (“DOJ”), which filed its first in 2020. The Justice Department later consolidated its lawsuit with those of 35 states, the territories of Puerto Rico and Guam, and Washington, D.C. The case went to trial in early September 2023 and should last approximately three months.

The Department of Justice filed its second antitrust complaint to break up Google’s advertising business in the country January 2023. Ministry of Justice announced April 17, 2023, which was joined by 17 states in the second complaint. An unfavorable ruling in either case could undercut Alphabet’s most profitable business, search advertising. Even if it receives a favorable ruling, the lawsuit could harm the company’s business compared to Problems faced by Microsoft During its long and difficult antitrust trial in 2001. The country also faces litigation in other parts of the world. The European Commission also wants to Kill the Google Ads business. And recently, the Japan Fair Trade Commission has done just that Started checking out Google Android Practice with smartphone manufacturers

Some of Alphabet’s competitors are licking their chops as they realize that anything that hurts Google’s ad business will help them. These companies include Microsoft, The Trade Desk (TTD), TikTok, Meta Platforms (MetaRocco (ROKU), magnet (MGNI), Snap (Snap), PubMatic (Pubm), big business (BIGC) and any other company that has a stake in the digital advertising market. As government regulators take a stand against Google, it should be easier for companies to break Google’s search monopoly.

Last but not least, although it may be difficult for any company to cross the Google moat without government help, the era of generative AI makes it possible for all companies to create AI chatbots. Companies like Meta Platforms have already developed 28 different chatbotsEach of them is specialized in different subjects and has different personalities. The sheer weight of all the chatbots entering the market from multiple companies could also erode Google’s search monopoly as people may prefer chatbots from other companies to answer different questions.

good news

All important metrics outside of Google Cloud were favorable. Alphabet’s biggest source of revenue, its advertising business, continues to recover after a terrible 2022. Google’s total advertising revenue grew 9% to $59.65 billion. Exceeding analysts’ estimates YouTube’s $59.12 billion in ad revenue grew 12% to nearly $8 billion, beating estimates for YouTube ad revenue of $7.82 billion.

Even better, Alphabet is no longer the company that spends money like a drunken sailor, as it did before interest rates rose. During the third-quarter earnings call, CFO Porat said Alphabet “is looking to grow revenue at a faster rate than expenses as we focus on delivering sustainable financial value.” That focus on cost control should help accelerate earnings growth again in 2023, which is partly behind the stock’s rally this year.

Finally, while the poor performance of the Cloud unit is a concern, investors should also consider that Alphabet has recently launched many of its AI cloud products that it announced at the show. Google Cloud Next 2023 The developer conference was held between August 2931. For example, the company just released Duet AI for Google Workspacea competitor for Microsoft Copilot, on August 29, two-thirds of the way through the third trimester. So, it may be too early to determine whether Alphabet’s cloud AI products will help it on Azure and AWS.

Suppose that Google Cloud’s AI products become attractive to customers after they get a chance to try them, and that economic improvements make customers less willing to pursue cloud cost savings. Sales growth for its cloud business could be satisfactory over the next three to five years. The market may have overreacted to Google Cloud’s lack of revenue and will quickly forget about the revenue loss if the company’s AI efforts pay off in the long run.

It devalues the stock market

The chart below shows Alphabet’s earnings per share (“EPS”) estimates between 2023 and 2028. The company has a 5-year EPS compounded annual growth rate of 17.36%.

Seeking Alpha

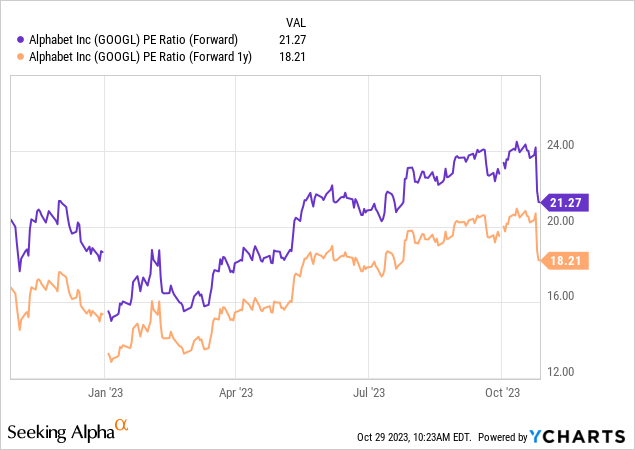

The company trades at a forward price-to-earnings (P/E) ratio of 21.22 and a one-year forward P/E ratio of 18.37, which is very low for a company of this quality. Let’s say the company has a good business model, a strong track record of execution, leadership in the rapidly expanding field of artificial intelligence, and a high double-digit EPS estimate over the next five years. Alphabet deserves a higher rating because of its EPS growth. The chart below shows the company’s forward P/E ratio.

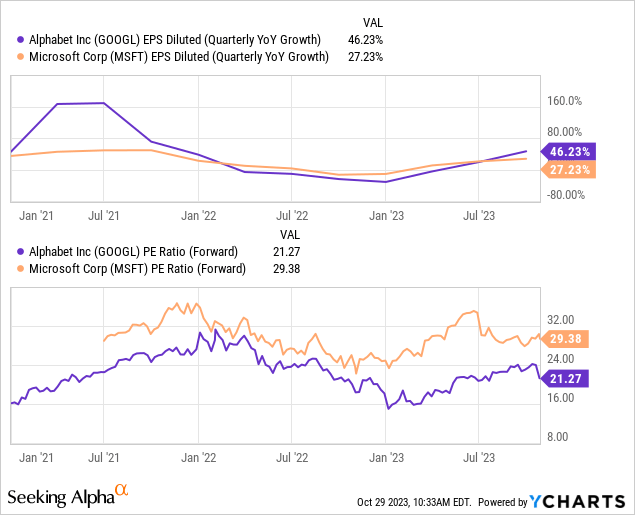

The chart below compares Microsoft’s and Alphabet’s EPS growth rates and forward P/E ratios. This comparison shows that while Alphabet posted a much higher EPS growth rate in the third quarter, Microsoft posted a much higher forward P/E ratio. While Microsoft deserves a higher valuation due to its stronger cloud numbers, Alphabet should trade at least a forward P/E of around 25. That valuation implies a share price of $143.59, a 17.5% premium to Alphabet’s Oct. 27 closing price of $122.17.

Last, the alphabet GF value $144.74 was 18% higher than the stock’s closing price on October 27, 2023, indicating that the market could modestly undervalue the stock. GF value is a proprietary calculation designed to measure the fair value of a stock.

Should you buy stocks?

Just two weeks ago, Alphabet’s stock hit a 52-week high of $142.38, up 60 percent on the year, and some investors were wondering if it was too late to invest. If you were one of those investors, the market has now given you another chance to add this AI leader to your portfolio. I recommend aggressive growth investors buy the stock at these levels.

#Google #Buy #Artificial #Intelligence #Company #Declining #Earnings #NASDAQGOOG

Image Source : seekingalpha.com